How to Redesign an App — Complete Guide with Recommendations from Devlight

An online queue, an online shopping system, online checkouts — building your own neobank is closely connected with features that seemed impossible only a dozen years ago. Financial institutions have long ago taken positions in the digital space since our lives have been drastically changed by factors such as

Many services have switched to a virtual format and work primarily online. Worldwide quarantine has shown that it is profitable and convenient. More and more areas are switching to remote customer service, banks included.

In practice, a neobank is a fintech company that provides banking services only in digital format: through a mobile application or website. Sounds simple, right? However, to build a neobank that will make clients trust their money to an entity having no tangible department, you will face a few exciting tasks and overcome some challenges. How to open a neobank in 2023? Let’s delve into this topic.

After you decide to develop a neobank, you automatically become the fintech player. Fintech is a generic term that applies to industries, organizations, and innovations, the expertise of which lies at the intersection of finance and technology. Fintech dates back to the late nineteenth – early twentieth century when the first Trans-Atlantic communications streamlined the processes of exchange of financial information and, thus, improved financial services.

Neobanks, otherwise known as challenger banks, or banking disruptors, are companies that are designed to provide banking services digitally, via web apps and other types of software, without any physical offices or contacts between the representatives. They are one of the fintech industry’s latest trends aimed at improving the fintech services making them fully accessible online.

There are more than 200 neobanks in the world now, and their number is going to grow, as it is quite a competitive and tough market where it is difficult for businesses to sustain themselves and cater to the client’s needs effectively. The market size of neo and challenger banks was estimated at nearly 47 billion U.S. dollars in 2021.

Neobanks began to develop recently but have already managed to win a large client base. This trend can be explained by a number of advantages offered by this type of fintech app. If your desire to build a neobank lacks specific arguments, we hurry to ensure you that such a business will be on top of market demand in the next decade. Why? Apart from switching their services fully online, neobanks also offer

The success of neobanks often depends on the regulatory environment and clients’ actual needs in a particular jurisdiction. At the moment, the most successful neobank launch stories are associated with Europe, where the UK is the leader among all countries.

Neobanks, sometimes referred to as “challenger banks,” usually specialize in specific services such as checking and savings accounts. They also tend to be more nimble and transparent than their mega-bank competitors in the financial industry, although many of them partner with such institutions to secure their financial products. However, since this niche has been developing quickly, some clear trends can be already highlighted. Before you start building your own neobank, pay attention to the next:

Traditional digital banking is always tied to the bank itself. Clients will still need to visit the offline bank establishment to sign papers or carry out some procedures. Building your own neobank means developing the digital interface to provide a fully virtual standard service set.

Besides, a neobank is always about the broad functionality of financial services, including but not limited to automatic income and expense reporting. It is an app more functional than most fintech startups we usually deal with. Mainly because a neobank is regulated by the same legislative base as a traditional bank or has to be in a partnership with a traditional bank that works as a banking services provider for the neobank’s clients.

The main idea of a successful neobank lies solely in market research of clients’ needs and providing painkilling functions by technically innovative means, even if the client wants to have a trading tool and parenting control features for junior banking in the same app. The concentration on satisfying customers’ needs is key to the neobank API.

In the global fintech market, customers have a broad selection of successful neobank apps. As developers who strive to build a neobank that would stand out, we follow the market leaders to highlight the features that make these apps special.

Our top-3 best neobanks apps list:

Revolut’s journey started in July 2015 at the Level39 tech accelerator in Canary Wharf. Last year, being the most significant financial unicorn in Great Britain, it raised Series E funding of $800m. More than 16m customers are happy to use this great financial tool.

The goal of Revolut is to become the world’s first truly global super app and provide access to financial services to everyone.

Features

Main points

Revolut’s owners definitely knew some secrets on how to start a neobank. The app is controversial in its marketing, PR, and HR branding, but it might be the way to get on the first lines of scandals, hypes, and trends. The ambition to satisfy all tech-savvy dynamic people with their financial tools brings to the market full of competitors: starting with traditional banks and ending with niche banking or money apps.

“Brazillian neobank giant” and “the most valuable Latin fintech” are typical synonyms for Nubank. And these descriptions are not empty words, as overcoming the new success milestone of 6m users and reporting a new record of profit in the latest quarter are good signs for the neobank business.

After some rounds of seeding investments, in early 2016, Nubank had 500.000+ users reaching their limits of operational capabilities and had more than 75.000+ future accounts queuing on the waiting list.

Features

This seemingly comprehensible and attainable set of features made Nubank the friendliest and most transparent bank that changed the image of the banking establishment in Brazil.

Main thoughts

Following the axioms of physics, things are doing everything to stay in stillness and save the status quo. Still, the victory of such simple apps made by dynamic and stubborn companies like Nubank is unavoidable.

N26 is a European neobank paying attention to digital security and achieving full compliance with European financial regulations. It is fully recognized as a regular bank in the Eurozone and currently has more than 5m customers worldwide. Starting from 2013, N26 has been through various difficulties developing and balancing the app under the circumstances of high competition, a heavily regulated Eurozone, and a community of whimsy users with high demands.

Do you want to develop a neobank like N26? Let’s see what makes it #1 for its customers.

Features

Main outcomes

The N26 has become a child of old Europe and a dream of digitalization: pursuing the ideals of bureaucracy, lobbying of interests of current banking market participants, but still motivated by its own customers to break the old rules. Reliability is tightly connected with security, so keeping customers assured of the safety of their assets is still a top priority.

You cannot take the best of each neobank and produce a Frankenstein monster of it without preparation and market research. Your audience deserves something special and customizable, and you have a different background than Revolut or Nubank. Still, you should develop a neobank with of a kind bearing these points in mind:

Neobank starts with a customer need and discomfort you can solve using technology. Then, the abstract hypothesis matures into a product idea and decomposes into scenarios of how it benefits the customer. The answer to “how” you have to do it—lies in the domain specificity.

How to open a neobank? The first and main challenge you must overcome to hit the neobank market is conducting Comprehensive Customer and Market Research. Get a list of fears and worries, nice-to-haves, and must-be features.

The most important high-level statements are tightly connected with the following questions you should answer before building your own neobank:

The ignorance of market and geographical targeting can cause a lot of twists and turns that were not planned and thus will multiply the cost of development. So in parallel with your audience research, select the market you want to compete in as you develop a neobank.

The maturity of the neobank markets of the world can vary depending on the region. The most developed and saturated markets are European, with visible leaders of Great Britain and Sweden neobanks, the USA, Brazil in the LATAM region, and South Korea.

To cope with regulatory obstacles, you must deal with powerful institutions and spend some time in rooms and corridors of bureaucracy. In the United States, the Office of the Comptroller of the Currency (OCC) within the United States Department of the Treasury checks and approves all emerging neobanks. In Europe, this is the European Banking Authority (EBA), another not-cheap and not-fast circumstance to deal with as you build a neobank.

There are two main principles for building secure infrastructures that are worth mentioning here:

Hiring security specialists to build up the security information and event management system (SIEM) that will automatically monitor and react to unexpected behavior due to the protocol is a must. Other actions you can take to make your development more security-aware and your whole neobank more attractive for your clients:

ISO 27001 standard: if you go through this certification, you will be in a league of neobanks that cover all FinTech data security standards. It is tough but worth it.

Interested? Eliminate any early-stage uncertainty.

After we mentioned the integrations part, we have come to the most interesting part of our research of how to start a neobank. Your company has to cover the heroic to-do list of bureaucratic regulations on the one hand and deal with all features development on the other.

The BaaS model of development is the most common one, as the cooperative model requires a tech-savvy bank partner which is not easy to find. Besides, to build a neobank using a platform model, be ready to provide investment and seek synergy of geniuses in programming and project management.

The biggest plus for the BaaS model is that they care about all connections with banks and licenses, transferring services, card emitting companies, and all those Visas and Mastercards for you. All connections are reliable and tested and can be customized with 3rd party providers for your convenience.

Another way of prioritizing features is by applying the Kano model. This framework is based on the simple thought that a feature has higher priority than another if it is clearly more desirable for the client. The price of implementation is also taken into account.

How to start a neobank based on the Kano model? Devlight team uses its modified version and categorizes features into three groups:

We have collected a general list of features for you to sort and group according to your special case:

| Typical features | Advanced features |

| Simple Onboarding | Stocks and cryptocurrencies |

| Personal account management | Accumulation system |

| Secure Authentication | Referral system |

| Customer support | Cost tracking |

| Transaction history | Dynamic CVV2 |

| Internet limits | Cashback |

| Payment templates | Two-factor authentication/ Biometrical authentication |

| Contact database synchronization | Buy Now Pay Later /Embedded Financing |

| Credit lines | Digital and HybridInvestments |

| Notification and reminder system | Digital Mortgages |

| Single-screen transfers | Gamification features |

| Real-time fraud detection | |

| ATM cash withdrawal | |

| QR payments |

How to open a neobank depending on the maturity of the market? Each of the advanced features can be simply moved to the basic section because the appetites of the audience grow with each new neobank launch.

Your architecture will be unique. As the blueprints differ from person to person, your architecture will differ from each already existing one. We can just describe some of them for you and explain what is common for all of them.

Simple architecture example

As you develop a neobank, you should make sure it works safely, fast, is efficient and stays error-prone. So all knots of integrations, ETL (extract, load, transform) processes, recording, and storing sides should be reliable and secure.

Another important point to consider from the very beginning is scalability. Without layers that will provide you with readiness for any traffic, the app’s security and reliability will equal zero.

| App side | Server side |

| It is only a wrapper for a client to access the functions from the server side | All server capacities involved in the project are here computing, running, and sending answers to the app side |

| Authentification | Authorization |

| Biometric data reader | API endpoints |

| User-persistent storage | Calculations |

| Fancy UI | 3rd party integrations |

| Data visualization | Monitoring |

| Notifications | Data storage |

| Notifications | |

| POTENTIALLY VULNERABLE PART | POTENTIALLY SECURE PART |

An important part of learning how to open a neobank is choosing the specialization and the way of being profitable according to your market and target audience. Neobanks acquire clients faster than traditional ones, but the end revenue is still smaller.

The ways to generate profit include

You may not know that, but building your own neobank isn’t just coming up with the newest tools and the most expensive development services from the beginning. Be mindful of your dev journey, as it is a marathon, not a sprint. Even if you have already won a round or two of investments, you should be mindful of each new tool bought for your team to use. App Development approaches:

| Native | Cross-platform |

| Each platform is a separate codebase and team of devs | Same codebase for all platforms |

| Best native integration with direct access to the device API | Native integration could be cumbersome, but it is possible to do it right |

| Consistent UI (may be customized in all platforms separate iterations) | Limited consistency, but it is not a problem with a fully custom UI, not the native |

| Best possible performance and 100% successful launch on particular devices, but the list of them is quite limited | Some of the app elements may not be compared with native elements in performance, but overall it is only a matter of testing to look good at the list of targeted devices. |

| iOS: Swift, Objective-C, Android: Kotlin, Java | Flutter, Kotlin Multi native, React Native, Cordova, Qt/Felgo |

Choosing a cross-platform or native approach depends greatly on your customer’s habits. If 99,9% of them use iOS and you plan mobile apps only, you shouldn’t even think about cross-platform.

This is the most painful part of our guide, so we will try to be as delicate as possible here. The price for a neobank launch may vary drastically depending on

The price you pay will always be less painful if your business is profitable. As most fintech startups, and neobanks in particular, struggle with their business models and revenue schemas, you must thoroughly think over your neobank API.

From the very beginning of development, each of your team members will have more than one role. After a few sleepless nights, your colleagues will start delegating and sharing their responsibilities.

As per Conway’s law, a system’s technical boundaries will reflect the organization’s structure. So, if an organization is built more around verticals that are oriented around features or services, the software systems will also reflect this.

Core: Founders’ Team

These people are energy core and inspiration machines for the neobank. They also become public personas typically, so all scandals and bumps will hit their reputation if something goes wrong:

Head’s Level

These guys know what to do with each vision of the Founder’s Team. Such professionals are key managers for all branches of the company. Their synchronization is a key to quick development and high quality of the final product.

Development Team

This is where the true jewels are hiding. People that will perform all the created tasks and make your neobank possible to appear on your client’s screen. Your core players of this game.

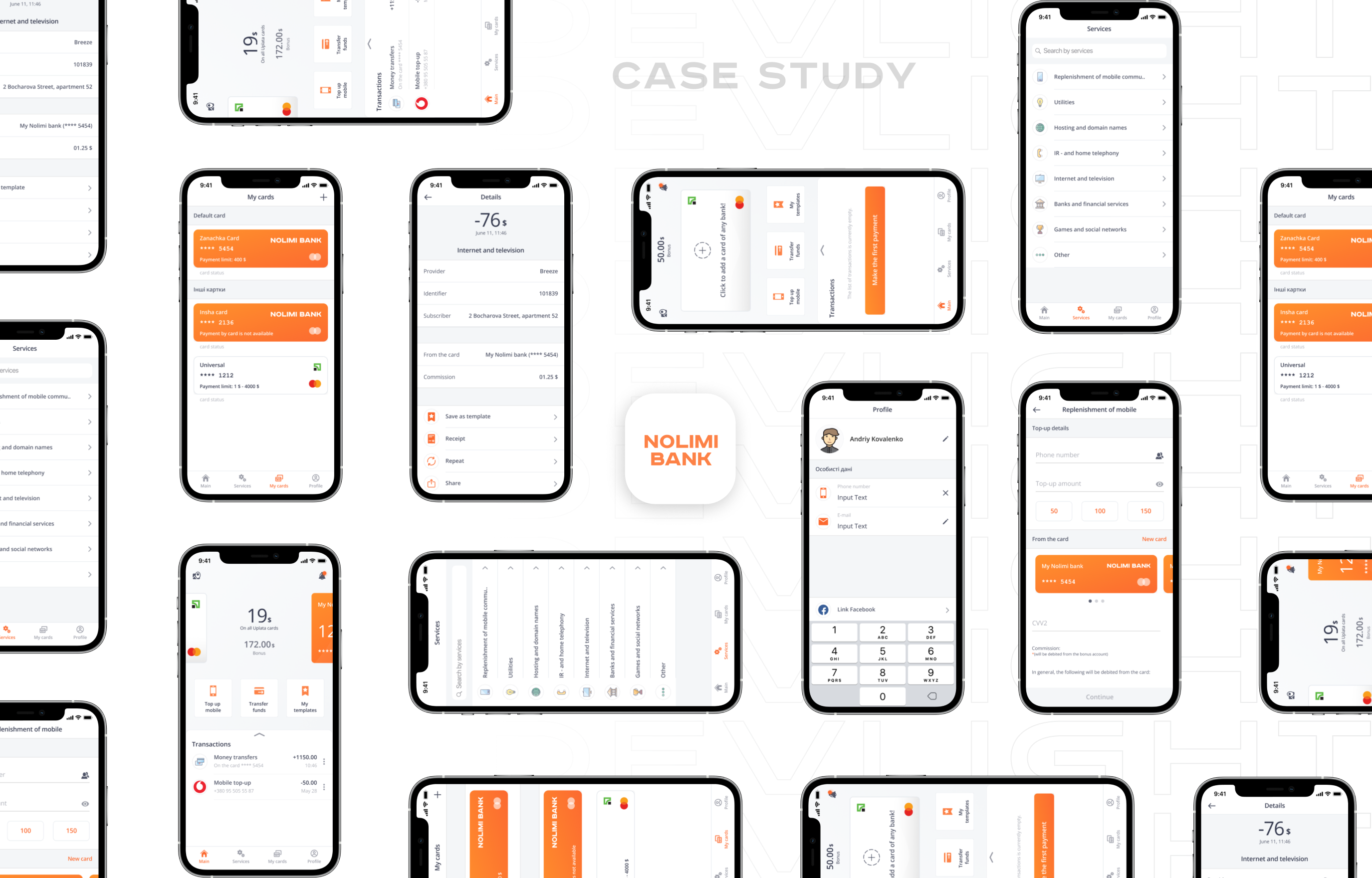

In the simplest of terms, your neobank is a technical savvy layer between banking functions set and a customer. A full-fledged neobank may cover the need for more than 90 back-end applications, 4 mobile applications, and 10 web applications, as in the case of Revolut.

The simplest lifecycle of the feature while building your own neobank has a defined set of stages:

You may say that it is a classic “waterfall,” but such a linear base fits easily within any Agile/ Scrum application development methodology. But remember that these instruments are created to simplify developers’ and project managers’ lives. For example, prioritizing the feature tasks can turn many devs’ problems into not-problems-at-all.

| Company name | Vodafone Ukraine |

| Niche | Telecommunications, internet |

| Main request | Enter the neobank market |

| Main challenge | Building the viable business idea from scratch |

| Deadline to the MVP | 2.5 months |

It was 2020, the first lockdown after COVID-19 pandemics has hit the world economy. Each business had to adapt to the new circumstances and stay profitable. And missions to discover new markets become not a benefit, but a chance to survive and enforce the business.

One of the largest telecommunication company in the world, Vodafone, has come to us with a bare wish to build up an app in the quite new market for them. Thanks to the strong product development expertise, we assess the market quickly and find the best-matching app idea according to our clients’ requirements and limitations.

Thanks to the Discovery phase of our service-providing model, we can pull the business insights out of data shredded over the niche as we at Devlight are mostly interested in building viable products, not just lines of code.

Request

Vodafone asked us to find a competitive set of services that can be wrapped in the app that will fit the market and deserve the customers’ love and everyday use. The client wanted to diversify its services and strengthen its position as a multi-market company.

As Vodafone assessed the fintech industry as quite new for them, they wanted to hear more suggestions from us on where they have to focus. So our task is logically divided into two parts:

Limitations and challenges

Because of the pandemic, we had to provide 100% of our services online with no discount for quality. We conducted 40+ hours of online conferences, meetings, and in-depth interviews. According to the client’s deadline, we have had only 2.5 months for all we have planned. But treasures are born under high pressure — from stars to diamonds.

After a few investigation sessions with a client, another strict limitation we have got was that Vodafone wanted to avoid any crediting services in the app’s services portfolio. That motivated us to find another business solution for the neobanking experience that would fit Vodafone and generate a stable income.

Process

To build a neobank by forging the right solution for the client, Devlight uses a two-phased process of Product Discovery and Product Development, as both processes are inseparable. This is the reason for the viability of our products and their popularity with millions of customers who use our products every day.

In this particular case, here is a detailed action list of what has been done for Vodafone to complete the task.

Solution

After dealing with each task from the Product Discovery phase, we ended up with a set of outcomes for our customer:

Competitors’ research is an efficient instrument for positioning and market discovery. It’s a must-be stage of our product development.

After analyzing what’s under the hood in competitors’ products, we’re able to create our own features backlog to get a helicopter view of all things that must be done in development.

It’s design time! We prototype the main screens and their possible variants of them to select the most fitting vector for our design system. Few options of design are going through our targeted audience reviews to check if it’s clear and understandable for them.

It is an excellent visual tool that describes the value proposition of product, its structure, customers, and the financial part of business. This diagram allows you to document the entire shape of your business model.

Vodafone was pleased with the prototype and business model that we developed for their project. We found a way to build a neobank that would land a telecommunications giant on a completely new market based on a tested and prototyped viable service.

Traditional banks are already forced to respond to changes in customer behavior and compete now not only with each other but also with fintech companies. A neobank API is not burdened by a giant employee base and capital costs but is still able to increase its market share quickly.

The sooner you as a business owner realize the changes that are taking place and start building your own neobank, the more likely you will survive. The quicker you succeed in the digitalized world, the more opportunities consumers will receive. Build a neobank to offer your audience a better product at a better price. And for new entrepreneurs, all these trends serve as a great opportunity to start building the business of the future immediately.

Interchange is the most popular monetization model used by neobanks. The merchants repay the neobanking app a sum spent by customers who were using debit cards. As a neobank owner, you can also offer different subscription options to your users: premium features, AI helpers, marketplace services, and paid memberships.

GOT A PROJECT IN MIND?